When it comes to paying for your insurance, most people default to monthly payments. It feels easier, more manageable, and less stressful on the wallet. But here is the part many do not realize: choosing monthly billing could actually be increasing the total amount you pay over time.

Let’s break it down in simple terms so you can decide what is best for your situation.

Why Monthly Payments Feel Easier (But Are not Always Cheaper)

Monthly billing is popular for a reason it spreads the cost out. Instead of paying a large amount upfront, you divide your premium into smaller, predictable payments.

But convenience often comes at a cost.

Insurance companies typically add installment or service fees when you choose to pay monthly. These fees might seem small sometimes just a few dollars per payment but over a full policy term, they add up.

On top of that, some carriers apply a slightly higher rate structure to monthly billing because they are taking on more administrative work and payment risk.

What Happens When You Pay Annually?

When you pay your premium in full upfront (annually or semi-annually), you remove a lot of those extra costs.

Here is what that can mean for you:

- No installment fees

- Lower overall premium in many cases

- Fewer chances of missed or returned payments

- Less risk of policy cancellation due to billing issues

In short, you are simplifying the process—and often saving money in the long run.

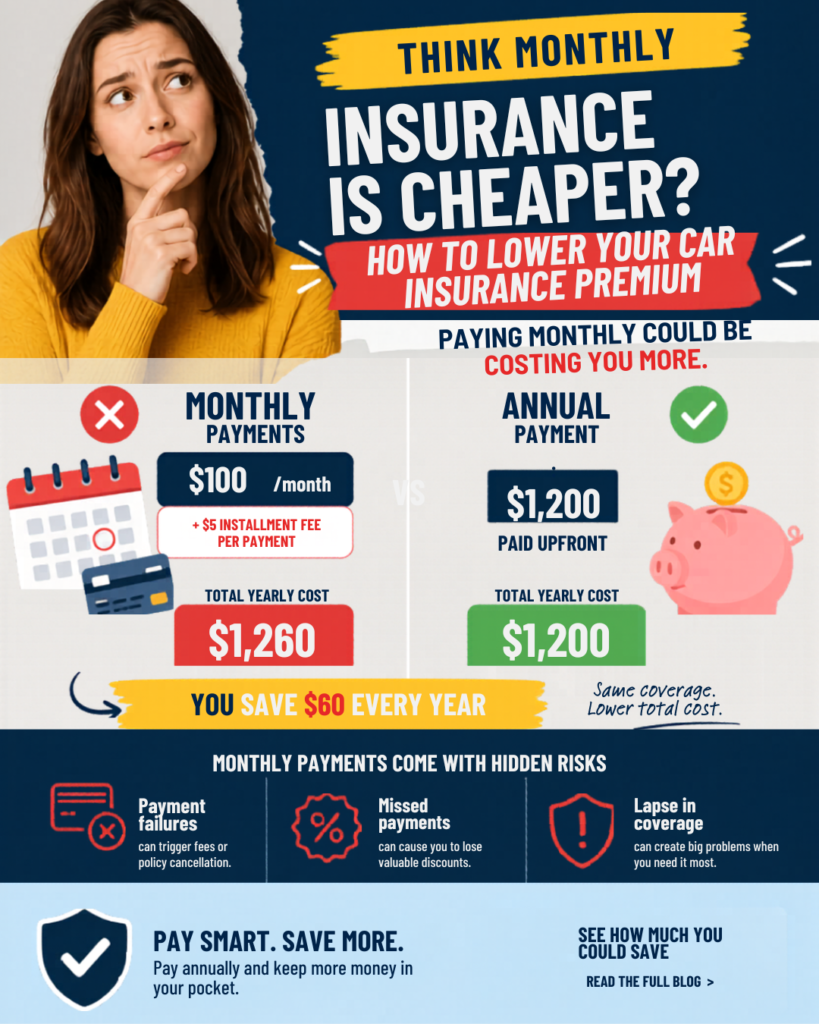

The Real Cost Difference: Monthly vs. Annual

Let’s say your policy costs $1,200 per year.

- Monthly billing:

$100/month + $5 installment fee = $105/month

Total yearly cost = $1,260 - Annual billing:

$1,200 paid upfront

Total yearly cost = $1,200

That is a $60 difference for the exact same coverage.

Now multiply that across multiple policies—auto, home, renters—and the savings can become significant.

Other Hidden Risks of Monthly Payments

Beyond the added cost, monthly billing can create other issues many people do not think about:

1. Payment Failures

If a payment gets declined (expired card, insufficient funds, etc.), it can trigger late fees or even policy cancellation.

2. Lost Discounts

Some discounts—like autopay or responsible payer—can fall off if a payment fails, increasing your premium mid-policy.

3. Coverage Gaps

Missed payments can lead to a lapse in coverage, which can cause problems with lenders, landlords, or even your state requirements.

When Monthly Payments Still Make Sense

To be fair, annual billing is not for everyone.

Monthly payments can still be the better option if:

- Paying in full would strain your cash flow

- You prefer budgeting smaller, consistent amounts

- You are managing multiple financial priorities at once

The key is not that monthly is “bad”—it is that many people do not realize the trade-off.

A Smarter Approach: Find the Balance

If paying annually is not realistic right now, here are a few ways to reduce the extra cost:

- Ask about semi-annual or quarterly billing (often lower fees than monthly)

- Set up automatic payments to avoid missed payments and keep discounts

- Review your policy regularly to make sure you are not overpaying elsewhere

The Bottom Line

Monthly payments offer convenience but that convenience often comes with added costs and risks. Paying your insurance premium annually can reduce fees, simplify your billing, and potentially save you money over time.

If you are not sure which option is best for you, it is worth reviewing your current billing setup. A quick conversation can reveal opportunities to save—without sacrificing coverage.

Want to see if switching your billing option could lower your total premium?

Reach out for a quick policy review—we all walk you through your options and help you make the most cost-effective choice.